The global pharmaceutical contract development and manufacturing organization (CDMO) market was valued at an estimated USD 146.0 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 7.2% from 2024 to 2030. The market's growth is largely due to increasing investments by CDMOs in new drug development, alongside rising demand for innovative therapies. Factors like heightened pharmaceutical research and development (R&D) spending, demand for genetic drugs, a higher prevalence of cancer and age-related disorders, and the need for advanced therapeutic solutions are driving market expansion.

Furthermore, the growth of biosimilars, biologics, personalized medicine, orphan drugs, companion diagnostics, and adaptive trial designs is likely to amplify demand for CDMO services. As companies explore novel areas, the growing need for regulatory compliance boosts demand for specialized CDMO providers skilled in both development and manufacturing processes.

Gather more insights about the market drivers, restrains and growth of the Global Pharmaceutical CDMO Market

Strategic initiatives by companies are also expected to support market growth. For instance, in January 2022, Lonza partnered with HaemaLogiX to produce KappaMab, a monoclonal antibody drug candidate for myeloma. Similarly, in December 2023, Innovent Biologics expanded its licensing deal with Synaffix B.V., a Lonza subsidiary, to further develop its antibody-drug conjugate (ADC) platform technology. Such collaborations in biopharmaceutical development are expected to fuel CDMO market expansion.

In the pharmaceutical sector, speed-to-clinic and innovation are crucial, with small and specialty companies increasingly relying on third-party providers to meet industry demands. Many contract research organizations (CROs) and CDMOs operate a "one-stop-shop" model, offering comprehensive services from active pharmaceutical ingredient (API) development through commercialization. CDMOs employ diverse technologies and specialized skills to meet various product development challenges. However, significant differences in design capabilities exist among CDMOs, which can impact the ability to scale and commercialize products.

CDMOs with a broad range of technology proficiencies can meet diverse customer needs, and clients are increasingly willing to pay more for reliable, high-quality services. Major pharmaceutical companies, aiming to simplify their supply chains, encourage CDMOs to provide integrated solutions that cover multiple processes seamlessly along the value chain.

Application Insights

In 2023, the oncology segment led the market with a 21.82% revenue share and is anticipated to grow at a CAGR of 8.1% from 2024 to 2030. Applications within the market span oncology, infectious diseases, neurological disorders, and more. The oncology segment, which includes small molecules and biologics, has seen substantial growth due to rising cancer cases, demand for advanced treatments, and favorable regulatory pathways. The progress in personalized medicine and targeted therapies has transformed cancer treatment, enhancing efficacy and minimizing side effects. Increased R&D funding for biopharmaceuticals like monoclonal antibodies and ADCs to reduce the cancer burden is expected to drive revenue growth in this segment.

The infectious diseases segment is also experiencing strong growth due to an uptick in cases of hepatitis, cholera, measles, chickenpox, and typhoid, leading to increased demand for immunizations. Pharmaceutical CDMOs are actively involved in developing new therapies and drugs for diseases like hepatitis C, AIDS, Ebola, and norovirus, meeting the urgent need for new immunization solutions.

Product Insights

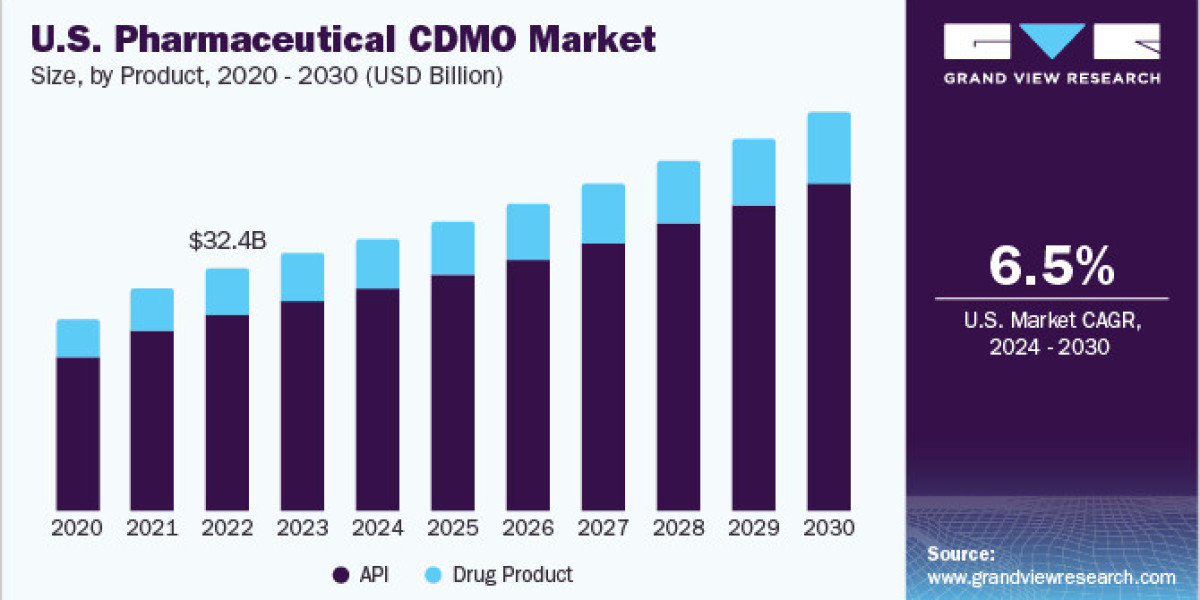

The active pharmaceutical ingredient (API) segment held the largest market share, at 81.20% in 2023, divided into APIs and drug products. APIs are further categorized by type, synthesis, drug, and manufacturing methods. Growth in this area is driven by increased demand for diverse formulations, new drug developments, and the widespread acceptance of these processes. Additionally, CDMOs are increasingly focused on new API formulations, contributing to the segment's expansion.

API types include traditional APIs, Highly Potent-API (HP-API), and biologics/large molecules, with traditional APIs anticipated to grow at a CAGR of 5.2% from 2024 to 2030 due to higher R&D activity, rising chronic disease rates, and growing demand for generics. The synthesis segment includes synthetic (solid & liquid) and biotech options. Meanwhile, the manufacturing segment, encompassing continuous and batch manufacturing, is projected to experience significant growth as CDMOs adopt continuous manufacturing methods to support pipeline drugs. The drug product segment, expected to grow at a robust CAGR, is supported by rising demand for various dose forms and an expanding R&D pipeline addressing global disease burdens.

Workflow Insights

The commercial segment led the market with an 87.93% revenue share in 2023, segmented into clinical and commercial categories. Growth in the commercial segment can be attributed to CDMOs' expertise in integrating advanced technologies and broadening their product portfolios. The ability to offer cost-effective, timely services further contributes to growth in this segment. The clinical segment’s growth is driven by increasing R&D for investigational drugs, alongside investments supporting innovation in drug development.

Order a free sample PDF of the Pharmaceutical CDMO Market Intelligence Study, published by Grand View Research.