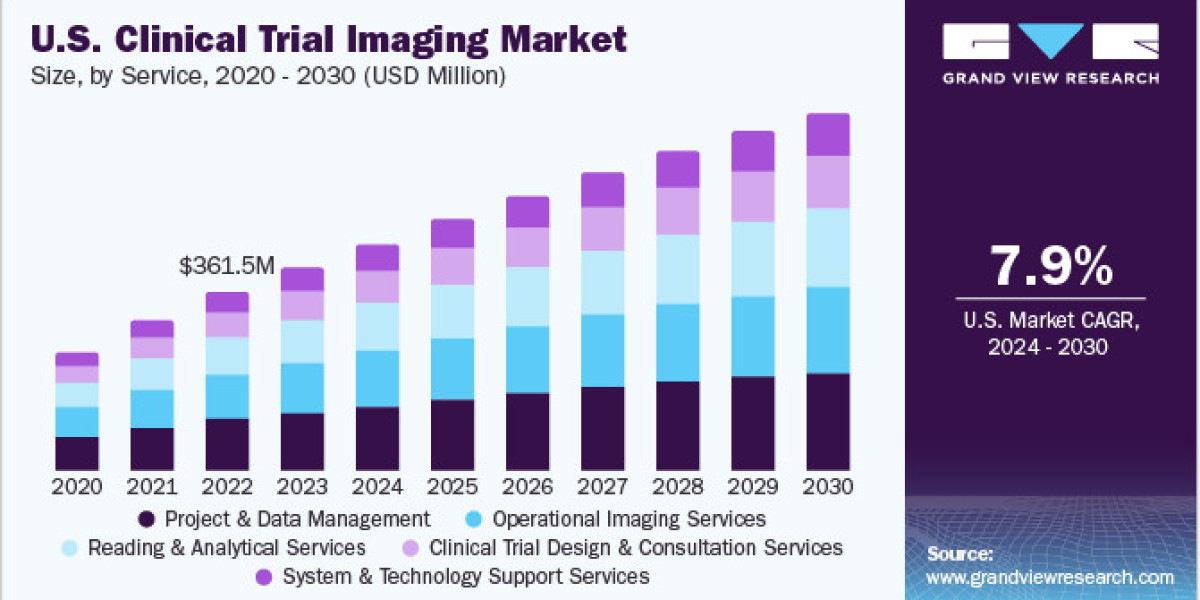

The global clinical trial imaging market was valued at approximately USD 1.14 billion in 2023 and is expected to expand at a compound annual growth rate (CAGR) of 7.60% from 2024 to 2030. This growth is driven by the burgeoning biotechnology and pharmaceutical sectors, along with increased investments in research and development focused on creating new treatments for various diseases. Medical imaging is essential in facilitating the development of innovative life science products.

Despite the rapidly evolving landscape of the medical imaging field, the biotechnology and pharmaceutical industries are experiencing consistent growth. This trend is largely attributable to heightened investments in medical imaging firms and a rise in mergers and acquisitions, which are integrating advanced imaging technologies to enhance clinical trials for medical devices.

Gather more insights about the market drivers, restrains and growth of the Global Clinical Trial Imaging Market

Technological advancements are significantly improving how clinical trial imaging data is collected, analyzed, and submitted. Technology-enabled imaging, particularly image analysis software, offers numerous advantages for clinical studies, including enhanced consistency, data accuracy, flexibility, and compliance. For example, image analysis software can guide and manage a reader by evaluating imaging time points. Additionally, the growing adoption of imaging technology, combined with more powerful computing capabilities, is expected to boost the role of imaging in clinical trials. The Quantitative Imaging Biomarkers Alliance (QIBA) has established standardized methods and procedures to ensure reliable and precise endpoints in clinical trials.

Segmentation Analysis:

Service Insights

In terms of services, project and data management services held the largest revenue share, accounting for 28.73% in 2023. Clinical trials that involve imaging require thorough data management and smooth coordination among various stakeholders. These services encompass a range of functions, including operational expertise, trial workflow development, project tracking, converting scans into digital formats, regulatory compliance, quality assurance, real-time reporting on trial progress, and the management of MRI centers. Moreover, the U.S. government has sanctioned a cloud-based server to protect all medical imaging records, including annotated and base images, ensuring security against natural disasters and facilitating quicker retrieval of these vital records.

Operational imaging services also represented a significant revenue share and are projected to experience the fastest CAGR of 7.32% from 2024 to 2030. These services include a variety of imaging modalities such as MRI, CT, ultrasound, OCT, PET, and SPECT, which are employed across multiple therapeutic areas including neurology, oncology, cardiovascular diseases, gastroenterology, musculoskeletal disorders, and medical device research for clinical trials. Imaging techniques are vital in clinical trials, providing critical evidence for informed decision-making. The Food and Drug Administration Modernization Act (FDAMA) of 1997 has facilitated the use of imaging modalities as essential tools in the development of medical devices and pharmaceuticals during clinical trials, allowing imaging data to be included in regulatory submissions, thus enhancing their role in the evaluation and approval process.

Modality Insights

By modality, the computed tomography (CT) scanners segment led the market with a revenue share of 29.13% in 2023. CT systems are widely utilized in clinical trial imaging due to their capability to generate detailed and precise images of internal body structures. CT scans use X-rays and computer processing to create cross-sectional images, enabling the identification and measurement of changes in tissues and organs over time. CT systems are non-invasive and relatively user-friendly, as they typically do not require contrast agents or radioactive substances, making them safer and more convenient for both patients and researchers. Researchers prefer CT scanners because they can generate substantial amounts of data quickly, which is essential for identifying trends and patterns across multiple patients.

The ultrasound segment is projected to grow at the highest CAGR of 8.01% from 2024 to 2030. Ultrasound devices are favored in the global market for their non-invasive nature and ability to provide real-time images of internal organs and tissues. They are particularly useful in researching cardiovascular diseases, oncology, and obstetrics. Ultrasound devices are preferred due to their safety and lack of harmful radiation. Additionally, they are portable, affordable, and easy to operate, making them ideal for clinical trial imaging. Notable ultrasound machines utilized in clinical trial imaging include the GE Healthcare LOGIQ E10, Philips Epiq Elite, and Siemens Healthineers ACUSON Sequoia.

Application Insights

Regarding applications, the oncology segment accounted for the largest revenue share of 28.98% in 2023. The high prevalence of cancer and the continuous demand for innovative therapies to treat various cancer types are driving market growth. Oncology trials often have complex imaging needs, requiring the assessment of tumor size, treatment response, and disease progression. Various imaging modalities, including CT scans, MRI, and PET scans, are employed to evaluate cancer treatment effectiveness. Advances in imaging technologies, such as PET-CT and functional MRI, have significantly enhanced the ability to visualize and assess tumors and their responses to treatment, making imaging integral to oncology trials. With the global cancer burden on the rise, the number of oncology clinical trials is expected to grow, further solidifying the oncology segment's dominance in the market.

The non-alcoholic steatohepatitis (NASH) segment is anticipated to experience the fastest CAGR of 9.75% during the forecast period. The increasing prevalence of NASH is driving segment growth, with studies indicating a global prevalence of 25.24%, highest in the Middle East and South America, and lowest in Africa. This prevalence is projected to rise to 63.0% by 2030, increasing the need for effective treatments. Consequently, companies are focusing on enhancing clinical trials to assess therapy effectiveness for NASH. Market players like ICON are employing data-driven strategies to optimize trial costs and timelines.

End-use Insights

In terms of end-use, the contract research organizations (CROs) segment led the market with a substantial revenue share of 45.95% in 2023. This dominance can be attributed to the rising costs associated with drug development and heightened research and development activities. Additionally, there is increasing demand from biotechnology and pharmaceutical companies for outsourcing research and development tasks to lower expenses. Collaborations with CROs also offer advanced services, prompting government organizations to prefer outsourcing projects to them.

The biotechnology and pharmaceutical segment is expected to witness the fastest CAGR of 7.97% during the forecast period. This rapid growth is driven by the need for developing new drugs and therapies to address chronic diseases. The increasing number of biotechnology and pharmaceutical firms is pushing manufacturers to deliver the most effective medications to end-users in a competitive landscape. Consequently, as innovative drug discoveries emerge, the demand for clinical trial imaging is projected to rise, further stimulating market growth.

Order a free sample PDF of the Clinical Trial Imaging Market Intelligence Study, published by Grand View Research.